For the last two years, the AI trade has been pretty straightforward: buy the chipmakers. NVIDIA (NVDA), AMD (AMD), Micron (MU) — these were the names that worked as capital rushed toward silicon. It was a K-shaped market, and the obvious winners kept winning.

But that trade is getting crowded. Valuations have stretched, money has poured into cap-weighted ETFs, and the market has started treating "AI" and "tech" as if they're the same thing. They're not.

The tech sector itself is now K-shaped. Just as the S&P 500 split between AI winners and everyone else, technology has fractured into multiple independent cycles. Owning "tech" isn't an investment thesis anymore — it's just a basket of businesses with completely different economic drivers.

You can see this divergence in ETF performance. The Technology Select Sector SPDR (XLK) is up 28.49% year-to-date, but that's largely because semiconductor giants dominate the index. Meanwhile, the iShares Expanded Tech-Software ETF (IGV) is down 12.4% year-to-date. And the VanEck Semiconductor ETF (SMH) is up 69.30% — completely decoupled from traditional enterprise tech.

The irony is that this first wave of AI winners may also be the easiest to identify. The next phase won't belong to the companies designing chips. It will belong to the firms solving the bottlenecks that prevent those chips from operating at full scale.

According to the State of the AI Economy report, AI demand is no longer speculative. Even after deducting circular transactions, annualized GenAI revenue has surpassed $175 billion. Hyperscalers have committed about $2 trillion in cumulative capital expenditure to build infrastructure. Demand continues to outpace supply across multiple layers — but the bottlenecks are increasingly physical, not computational.

Let's look at three of them.

Bottleneck #1: Advanced Packaging

Single-die silicon is hitting practical limits. Instead of making one enormous chip, manufacturers are stacking smaller chips together. This approach dramatically increases bandwidth while minimizing latency, but it requires sophisticated packaging technologies.

That shifts value toward the outsourced semiconductor assembly and test (OSAT) companies that actually integrate these designs. ASE Technology (ASX) is the global leader in advanced packaging volumes. Amkor Technology (AMKR) has become deeply embedded in high-performance computing and next-generation AI accelerators. Without advanced packaging, next-generation GPUs simply cannot be manufactured at scale.

Bottleneck #2: Moving Data

Training and inference clusters now contain tens of thousands of GPUs. Traditional copper networking becomes a constraint at higher speeds — power consumption and signal degradation rise sharply. So AI infrastructure is migrating toward optical interconnects capable of handling 800G today and eventually 1.6-terabit connections.

That creates an entirely different class of beneficiaries. Fabrinet (FN) manufactures many of the high-speed optical transceiver modules enabling these networks. Coherent Corp. (COHR) and Lumentum (LITE) provide critical optical components and photonics technology that have become increasingly important as NVIDIA's networking ecosystem expands.

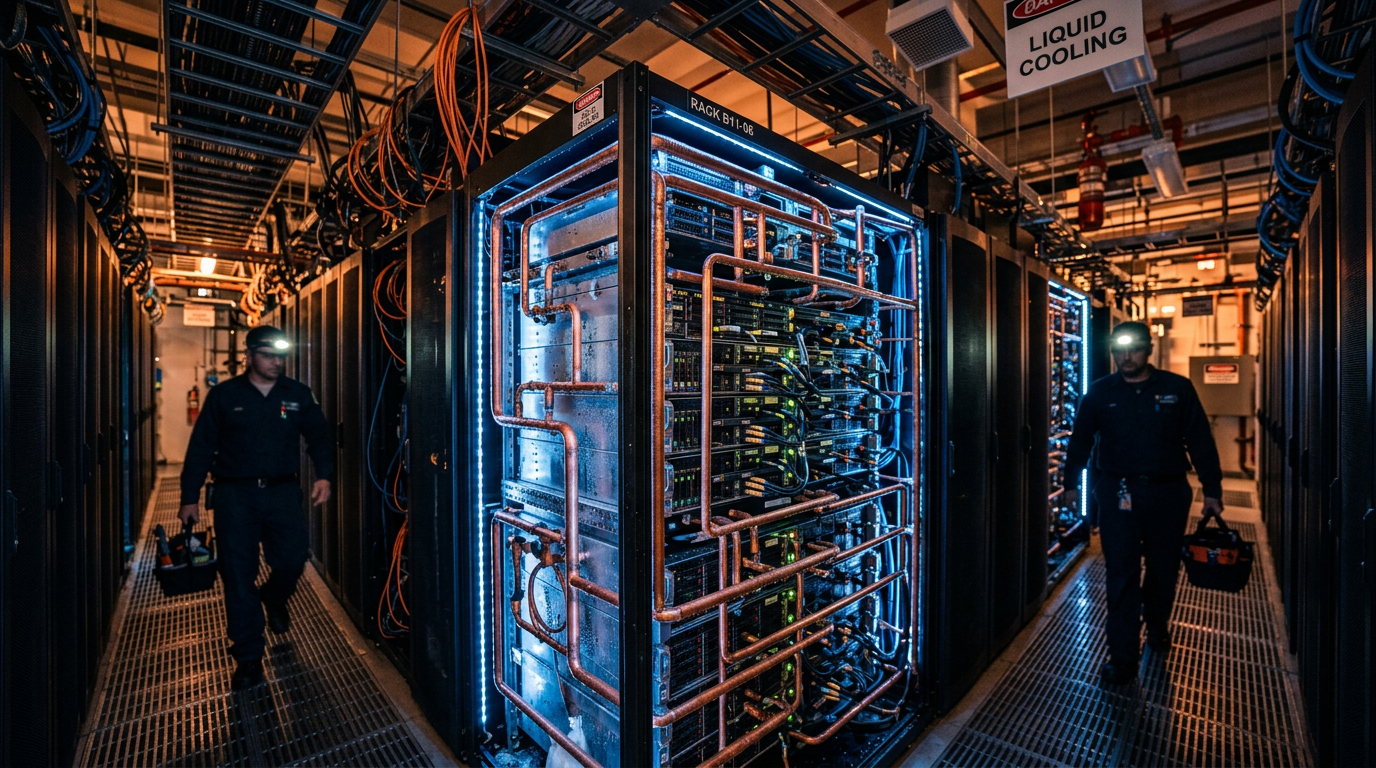

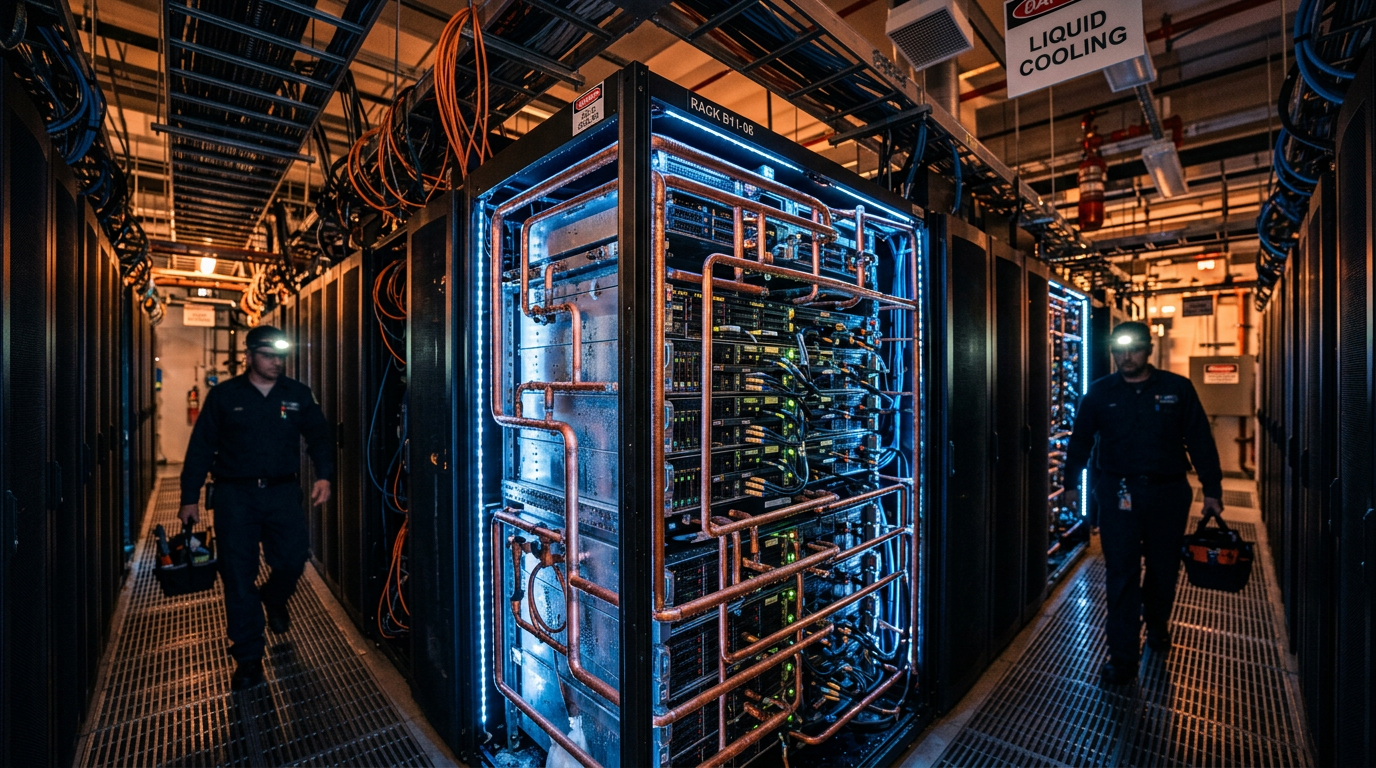

Bottleneck #3: Keeping Things Cool

This is the least glamorous opportunity — and maybe the most important. As AI server racks grow, the heat they generate is too much for air cooling. Direct-to-chip liquid cooling is transitioning from an optional upgrade to essential infrastructure.

Vertiv (VRT), a leader in liquid cooling, reported a record $15 billion backlog as companies race to deploy their tech. And Ecolab (ECL)'s $4.75 billion acquisition of CoolIT Systems shows how industrial water management is suddenly becoming part of the AI supply chain.

The chip trade was the first inning. The next wave belongs to the companies that make the chips actually work at scale.

.jpeg)